Insurance underwriters decide whether to provide insurance, and under what terms. They evaluate insurance applications and determine coverage amounts and premiums.

Duties

Insurance underwriters typically do the following:

- Analyze information stated on insurance applications

- Determine the risk involved in insuring a client

- Screen applicants on the basis of set criteria

- Evaluate recommendations from underwriting software

- Contact field representatives, medical personnel, and others to obtain further information

- Decide whether to offer insurance

- Determine appropriate premiums and amounts of coverage

- Review and update the rules that govern automation software

Underwriters are the main link between an insurance company and an insurance agent. Insurance underwriters use computer software programs to determine whether to approve an applicant. They take specific information about a client and enter it into a program. The program then provides recommendations on coverage and premiums. Underwriters evaluate these recommendations and decide whether to approve or reject the application. If a decision is difficult, they may consult additional sources, such as medical documents and credit scores.

For simple and common types of insurance, such as automobile insurance, underwriters can typically rely on automated recommendations. For more specific and complex insurance types, such as workers’ compensation, underwriters need to rely more on their own analytical insight.

Underwriters analyze the risk factors appearing on an application. For instance, if an applicant reports a previous bankruptcy, the underwriter must determine whether that information is relevant to the policy being applied for. The underwriter would likely consider how far in the past the bankruptcy occurred and how the applicant’s financial situation has changed since the applicant filed for bankruptcy.

Insurance underwriters must achieve a balance between risky and cautious decisions. If underwriters allow too much risk, the insurance company will pay out too many claims. But if they don’t approve enough applications, the company will not make enough money from premiums.

Most insurance underwriters specialize in one of three broad fields: life, health, and property and casualty. Although the job duties in each field are similar, the criteria that underwriters use vary. For example, for someone seeking life insurance, underwriters consider the person’s age and financial history. For someone applying for car insurance (a form of property and casualty insurance), underwriters consider the person’s driving record.

Within the broad field of property and casualty, underwriters may specialize even further into commercial (business) insurance or personal insurance. They may also specialize by the type of policy, such as for automobiles, boats (marine insurance), or homes (homeowners’ insurance).

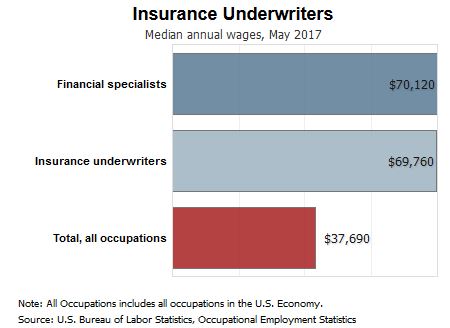

The median annual wage for insurance underwriters was $69,760 in May 2017. The median wage is the wage at which half the workers in an occupation earned more than that amount and half earned less. The lowest 10 percent earned less than $41,800, and the highest 10 percent earned more than $123,660.In May 2017, the median annual wages for insurance underwriters in the top industries in which they worked were as follows:

The median annual wage for insurance underwriters was $69,760 in May 2017. The median wage is the wage at which half the workers in an occupation earned more than that amount and half earned less. The lowest 10 percent earned less than $41,800, and the highest 10 percent earned more than $123,660.In May 2017, the median annual wages for insurance underwriters in the top industries in which they worked were as follows:

Note: All Occupations includes all occupations in the U.S. Economy.

Note: All Occupations includes all occupations in the U.S. Economy.